07 5440 5794

|

Investment mistakes cost you money – that’s why they must be avoided. What I’ve discovered over the years is there are only two ways to gaining the experience necessary to know how to avoid investment mistakes.

Frankly, I'm no glutton for punishment. The easy way makes sense to me. Avoid these mistakes, do better with your money and accelerate your journey to retirement happiness.

|

| Consider this window. Question: What happens when a rock is thrown at this window? Answer: The entire thing breaks. |  |

| Consider this window. Question: What happens when a rock is thrown at this window? Answer: 1/4 of the thing breaks. |  |

| Next, check out this window. Question: What happens when a rock is thrown at this window? Answer: 1/64th of the window breaks, hardly noticable. |  |

In the investment world, sometimes rocks get thrown.

And your investment portfolio can be a bit like a window.

When you only hold a few investments (or, only one), a well-aimed rock can bring the whole thing down.

We don’t know who will throw the rocks or where they’ll come from, but it’s a good idea to make sure that you are properly diversified, to reduce unnecessary risks like holding too few shares or just a single property.

Diversification helps to overcome that, and in turn produce a more stable and reliable return. Being well diversified also means you're positioned to capture the returns whenever and wherever they appear.

In my experience, more wealth is destroyed by poor diversification than any other cause.

And your investment portfolio can be a bit like a window.

When you only hold a few investments (or, only one), a well-aimed rock can bring the whole thing down.

We don’t know who will throw the rocks or where they’ll come from, but it’s a good idea to make sure that you are properly diversified, to reduce unnecessary risks like holding too few shares or just a single property.

Diversification helps to overcome that, and in turn produce a more stable and reliable return. Being well diversified also means you're positioned to capture the returns whenever and wherever they appear.

In my experience, more wealth is destroyed by poor diversification than any other cause.

KEY THOUGHT - Smart diversification reduces risk, preserves capital and produces more reliable returns

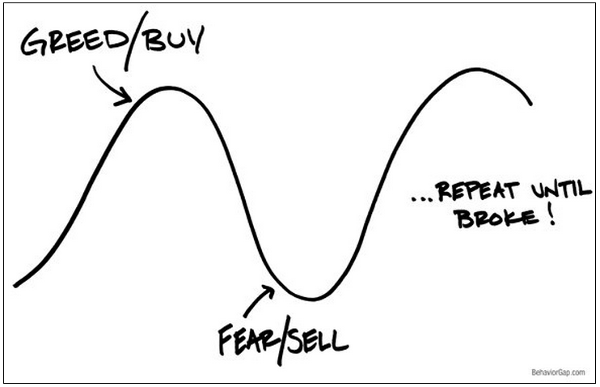

Mistake No. 3 - Not managing emotions

There’s little I can guarantee, but these things are true: Investment cycles always prevail eventually. Nothing goes in one direction forever. Trees don’t grow to the sky. Few things go to zero. And there’s little that’s as dangerous for investor health as insistence on assuming today’s events will continue into the foreseeable future.

It’s very difficult to convince yourself that;

a) The good times will eventually end OR

b) The bad times won’t last forever.

What this means is that we tend to panic when prices go down and we are over ambitious after a run-up in price.

My all-time favourite Behaviour Gap sketch by Carl Richards sums it up beautifully:

The truth is no-one knows what will happen next in investment markets.

Yes, some people do get lucky by making bets on certain shares and sectors or getting in or out at the right time or correctly guessing movements in interest rates or currencies.

But depending on luck is simply not a sustainable strategy.

The alternative approach to investment may not sound as exciting but is also a lot more reliable and a lot less work. It means reducing as far as possible the influence of fortune by taking a long-term and diversified approach.

Yes, some people do get lucky by making bets on certain shares and sectors or getting in or out at the right time or correctly guessing movements in interest rates or currencies.

But depending on luck is simply not a sustainable strategy.

The alternative approach to investment may not sound as exciting but is also a lot more reliable and a lot less work. It means reducing as far as possible the influence of fortune by taking a long-term and diversified approach.

KEY THOUGHT - Understand too that risk and return are intimately linked. You don’t get high returns without bearing some painful losses along the way. You cannot achieve perfect safety without accepting low returns.

Mistake No. 4 - Don't pay heed to fees and taxes

Costs and taxes matter. They matter a lot.

Day to day moves in the market are temporary, but costs are permanent. Over time, they can put a real dent in your wealth plans. That's why it makes sense to be mindful of fees and expenses.

Costs might include purchase costs or redemption costs, which means that you might pay money either going into or coming out of an investment.

In addition, many investment funds have ongoing expenses which are fees that come out of your investments. The fees feel invisible because you don't have to write a cheque for them. They're quietly deducted from your returns, but that doesn't make them any less real.

KEY THOUGHT – The value of your retirement fund responds to 3 variables. The investment return, how much you put in and what fees and taxes are taken out. Pay attention to all three at all times.

Mistake No. 5 - Not taking enough risk (or taking too much)

We Aussies are a successful bunch. Whether that be economically, on the sporting field or even how we get on with each other, we do most things really well. And we are super successful in the most important area of all – staying alive!

Thanks to skilled health care and a high standard of living, we just don’t die like we used to. In the future, we’ll be living even longer. The Government estimate that in 40 years’ time, life expectancy will be 95+ for men and 96+ for woman. Two million of us will be aged over 85. 40,000 of us will be over 100 - compared with 5,000 now and just 125 in 1975. Holy smoke, this really is the lucky country!!

Don’t fall into the trap of thinking you need to be very conservative with your investments as you approach retirement. Even when you do stop working, your retirement savings needs to last another 30 years or so, and those savings need to earn strong returns to ensure your money goes the distance.

That does not mean though that you should be making risky investments, be overleveraged or not sufficiently diversified.

This is not a one size fits all exercise and you need to think carefully about what are the optimal levels of risk for you, taking in to account how much money you have, how long it needs to last and how well you are going to sleep at night.

KEY THOUGHT - Our analysis of investment returns has found that maintaining some exposure to growth assets like shares and property is important for sustaining your income after retirement. Be sure to speak to a financial adviser to see what the impact on your asset allocation has on your future returns. These days, extended longevity and low returns from cash means you probably need a riskier portfolio longer than your parents did.

Conclusion

So, in a nutshell – get started, diversify, stay relaxed, recognise your limitations and avoid fees. Do these things, and you are far more likely to enjoy a successful investment experience.

Whenever you're ready....here are three ways I can help you get on track to a stress-free retirement.

1. Grab a copy of our free Ebook.

It's called “5 Money Must Do’s For The Over 50’s” and are the lessons learned from helping 1000’s of people find financial peace of mind over the last 30 years.

Whenever you're ready....here are three ways I can help you get on track to a stress-free retirement.

1. Grab a copy of our free Ebook.

It's called “5 Money Must Do’s For The Over 50’s” and are the lessons learned from helping 1000’s of people find financial peace of mind over the last 30 years.

2. Follow us on Facebook and Twitter and sign up to our regular emails updates.

They are great places for great ideas.

They are great places for great ideas.

3. Work directly with me.

If you’d like to work with me and my team to move from stressed and frustrated to relaxed and on track, you can schedule a phone call here. You’ll find out how we can help and if we are the right fit for you. 20 minutes, no obligation.

If you’d like to work with me and my team to move from stressed and frustrated to relaxed and on track, you can schedule a phone call here. You’ll find out how we can help and if we are the right fit for you. 20 minutes, no obligation.

IMPORTANT This information is of a general nature only and may not be relevant to your particular circumstances. It does not take your specific needs or circumstances into consideration, so you should look at your own financial position, objectives and requirements and seek financial advice before making any financial decisions.To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. See full Terms and Conditions here.

Jill P

1/7/2020 06:54:22 am

Hi Tony, you've confused me a little. You once told me that my super was very well diversified, but its really the only investment I have. So perhaps I'm not as diversified as I should be? Thanks Tony

15/7/2020 08:03:08 am

Hey there Jill, how have you been? You are very well diversified. Your super contains hundreds of different investments, so you'll be ready if there are a couple of rocks thrown :).

Your comment will be posted after it is approved.

RSS Feed

RSS Feed

30/6/2020

2 Comments